NFTs or Non-Fungible Tokens offer a secure way to verify ownership of a digital or non-digital asset. The NFTs are powered by blockchain technology.

NFTs are a relatively new concept. There is potential for NFTs to change the traditional markets as we know it.

The main benefit of NFTs is the decentralized nature of the technology. Instead of requiring a third party to trade assets, a peer-to-peer network does it for free in no time with unbreachable security.

Instead of using traditional money to trade NFTs, a cryptocurrency is used. You can buy and sell NFTs on NFT marketplaces.

During 2017-2021, NFTs went mainstream. A lot of digital art, such as music, videos, GIFs, and images are sold as NFTs on NFT marketplaces.

This complete guide teaches you how NFTs work. You will learn how blockchain technology works and how NFTs live in the blockchain. Besides, you will learn about different types of NFTs, NFT pros and cons, how to buy and sell NFTs, and much more.

This complete guide answers all of these and many more questions.

What Is an NFT?

NFT stands for non-fungible token. It is a digital certificate of authenticity.

An NFT is unique and it cannot be copied or replaced. An NFT lives in a blockchain, commonly the Ethereum blockchain. The entire network of nodes in the blockchain verifies the existence and the ownership of the NFT. There is no central authority needed.

At the moment, NFTs are popular in the form of digital arts. For example, a lot of images, music, and even sports moments are sold as NFTs. But an NFT can be used to digitally verify the ownership of anything, such as a car, real estate, and more.

If you purchase an NFT, you become the true owner of the NFT and the asset associated with it. NFT is like a one-of-a-kind playing card. There is only one copy and one owner verified by a big peer-to-peer network.

Let’s start understanding the NFT technology by making sense of the name “Non-Fungible Token”. More specifically, let’s take a look at the words “fungible” and “non-fungible” with a real-life example.

Fungible vs Non-Fungible

Your pet is an example of something being non-fungible. This is because another identical pet cannot replace your beloved one, even though it was the same breed and looked the same. Your pet is unique and there is only one of them in the entire universe.

On the other hand, a one-dollar bill is fungible. You can swap a dollar bill with another without noticing or losing value.

Now that you understand what fungibility and non-fungibility mean, let’s pay attention to the last word, token.

What Is a Token?

When talking about NFTs, the word token refers to a cryptocurrency or crypto asset living on a blockchain. Basically, a token is a node in the blockchain formed by other similar nodes. Each node has a unique ID and other data securely verified by the entire blockchain network.

Usually, NFTs live in the Ethereum blockchain. But these days there are loads of other blockchains you can find NFTs in.

To put it short, an NFT is a unique node in a blockchain. The word “non-fungible” refers to uniqueness, and the word “token” refers to the fact that it’s a node in a blockchain.

Now that you understand what the name NFT means on a high level, let’s dig deeper into the technical aspects by taking a closer look at NFT technology and blockchains. By the way, if you are not after the technical details of NFTs, feel free to skip this section. There is a lot of useful non-technical insight about NFTs to come.

Deep Dive: How Do NFTs Work?

An NFT is a digital proof of ownership that lives in the blockchain. This ownership can refer to something digital or non-digital. The idea of an NFT is there is no need for central authorities to verify ownership. Instead, a decentralized peer-to-peer network takes care of that. This makes the verification more secure, less prone to errors, and cheaper.

If you are unfamiliar with blockchains, it’s important to understand how they work to understand how NFTs work.

In case you are familiar with blockchain technology and cryptocurrencies, you can skip the following section.

But I’m sure a lot of people unfamiliar with NFTs don’t know anything about blockchains either. Here is a quick primer on blockchain technology that powers NFTs and cryptocurrencies.

What Is a Blockchain?

Blockchain technology powers cryptocurrencies and NFTs.

A cryptocurrency works such that there is a public ledger that is distributed across a big peer-to-peer network of computers. Each computer in this network has its own version of the ledger. For a transaction to be successful, all the computers in the network need to agree on the legitimacy of the transaction.

The system that organizes the public ledger is called a blockchain. Blockchain is a secure system that stores transactions in a way that is impossible to hack or change.

Blockchain technology is the driving force of cryptocurrencies and NFTs. Cryptos like Bitcoin and Ethereum operate on blockchain technology.

A blockchain is a digital ledger shared among an entire network of computers running the blockchain. The idea is that the network of computers verifies each transaction in the blockchain. This makes the system transparent and secure. Any computer can be part of the blockchain—even yours!

Even though the Google Docs analogy demonstrates the decentralized and transparent nature of blockchains, there is a key difference too. In a Google Docs file, you can overwrite original content. But on a blockchain, you cannot modify data inserted. This is what makes a blockchain secure.

The blocks in the blockchain are encrypted which makes it safe. The encryption guarantees one cannot read the data of the blocks without permission.

How Does a Blockchain Work?

Blockchain technology is powered by these three technologies:

- Cryptographic keys

- A shared ledger powered by a peer-to-peer network

- Computational power to store transactions and records

Cryptography makes it possible to do transactions securely and reliably between two parties. In cryptography, you have two keys: a public key and a private key. These keys are used to form a secure digital identity reference or “digital signature”. The digital signature is an integral part of blockchain technology because it allows for authorizing and controlling transactions.

A peer-to-peer network is a huge number of individuals in the blockchain that act as the decentralized authority to agree on the transactions in the blockchain. To do this, the P2P network uses digital signatures. To authorize a deal, a mathematical verification needs to take place. Once the verification is completed, the transaction between the two parties succeeds. The information of this transaction is stored in a block of a blockchain and remains there untouched forever.

This is a high-level description of how a blockchain works. To understand it better, let’s take a little bit closer look at the blocks that make up the blockchain. A blockchain has three integral parts that make it work:

- Blocks

- Nodes

- Miners

What Is a Block?

As the name blockchain suggests, it is a chain of blocks that represent transactions.

Each block in the blockchain is associated with three elements:

- Data. This is the transaction data in the block. It’s information about the recent transactions made using the blockchain. This data isn’t found in any other blocks. It’s like a page of a ledger.

- Nonce. Nonce or number used only once is a randomly generated 32-bit number. Once a new block is generated, a nonce is attached to the block. The nonce is used to generate a secure hash value to the block.

- Hash. The hash is a 256-bit number that is generated for each block using the nonce.

To take home, a block is a secure node in the blockchain protected by a hash value which makes it impossible to breach.

But who adds the blocks to the blockchain?

This is where miners help. The blockchain miners are responsible for adding blocks to the blockchain and thus adding more currency to the system.

What is a Blockchain Miner?

In blockchain technology, the miners are responsible for verifying transactions and mining new cryptocurrency for the market.

Each block in the blockchain consists of transaction data of approved transactions by the P2P network. Before adding a new block to the blockchain, the transactions in the block need to be approved. Because there is no central authority to do this, it’s the P2P network that does.

Verifying the transactions in a new blockchain block is called mining. The idea of mining is to use computational power to verify the legitimacy of transactions. But this increases the electricity bill as the computational power needed is high.

So is this some kind of voluntary work from the network?

Nope!

As a reward for successfully approving a new block to the blockchain, the miner gets a token. This is a small amount of cryptocurrency. This compensates for the work done in approving the block in the blockchain.

Notice that the reward is a new piece of cryptocurrency that gets generated upon verifying the block. This is why the process is called crypto mining. The miners mine more cryptocurrency for the blockchain system.

Who Can Mine Blockchains?

Any computer can become a miner on the blockchain. Although the computational power needed to successfully mine a block is astronomical.

Because the power required is so high, crypto mining usually takes place in mining pools that combine a bunch of computers’ computational power. These pools then share the rewards among the miners based on the amount of work each computer did.

Miners Solve the Double-Spending Problem

The blockchain miners approve transactions in the blockchain. But why is mining needed? Why not just add the transactions directly to the chain of blocks?

Blockchain miners solve the “double-spending problem” of cryptocurrency. Double-spending isn’t an issue with physical currency, but it’s a real problem with digital currency.

For example, a Bitcoin owner could spend the same Bitcoin twice if no verification mechanism was used.

There is a good real-life analogy as to what the miners do to verify transactions in a blockchain.

Imagine you have a $10 dollar bill and you create a counterfeit one. You spend the real bill in the grocery store and the counterfeit one in the apparel store. To get caught, someone would need to take the trouble of looking at the serial numbers of both bills. If the numbers match, it means one of the bills must be counterfeit.

The idea behind blockchain mining is the same. A miner makes sure no unit of digital currency is spent twice. If a miner is able to verify a transaction, they get a token as a reward. This token is also called cryptocurrency.

The mining process is all about guesswork. The miner tries to come up with a number that matches a target hash. This is basically like guessing a password. It requires a ton of computational power and repetitions. But no complex math is involved unlike many guides claim.

Now that you understand how blockchains and cryptos work, let’s talk about NFTs and blockchains.

NFTs Live on Blockchains

NFT or Non-Fungible Token is a special type of token that lives in a blockchain.

Typically, an NFT lives in the Ethereum blockchain but there are other blockchains for NFTs too.

Creating a new NFT is called minting. On a high level, the minting process works like this:

- A new block is generated into the blockchain.

- The information in the block is validated.

- The information is recorded in the blockchain.

The minting happens by running a piece of code called a smart contract in the blockchain. The smart contract code assigns ownership and handles the transferability of the NFT.

As you learned in the previous chapter, this sounds a lot like verifying transactions in a blockchain. As a matter of fact, adding a new NFT to a blockchain is a transaction! The entire P2P network must agree upon the transaction before the new NFT is minted.

An NFT is a unique token that cannot be replaced by another token in the blockchain. Notice that cryptocurrencies are not NFTs, because they are fungible. One Bitcoin can be replaced by another and you still end up having one Bitcoin. But you cannot replace an NFT with another because they are characterized by unique IDs that make them unchangeable.

Also, unlike cryptocurrencies, NFTs are indivisible. You cannot split the ownership of an NFT. There can be only one owner of an NFT.

NFT is a digitally verified representation of a digital or non-digital object, such as an image, video, deed to a car, or real estate.

What Gives NFT a Value?

The value of an NFT is tied to the asset it represents.

If the NFT represents something tangible, such as real estate, the pricing of the real estate is typically reflected in the price of the NFT.

If the NFT represents something with no real-life value, then its value is 100% speculative. For example, an NFT of a social media post, image, or video is about speculation. This is because there is no real-life value for a social media post, for example. A social-media-post-NFT might get its value based on the popularity of the author and the content of the post.

A cool part of the speculative value of NFT is the fact that there is a tiny chance of selling at a massive price.

For example, Twitter CEO Jack Dorsey sold his first Tweet at a whopping $2.9 million. Yet the bidding prices started as low as $1 three months prior to the transaction. This highlights that as long as there is interest and hype, a piece of NFT can grow sky-high.

Generally speaking, the value of NFT comes from factors like rarity, social proof, ownership, and utility.

The owner of the NFT can set the price as high or low as they want. Whether someone is going to buy it or not depends on many factors.

10 Common NFT Types

NFTs are used to digitally verify ownership of something digital or non-digital.

In a sense, anything can be an NFT.

Because NFT is a new concept, there is a lot of room for research, innovation, and improvements.

A key part of understanding what NFTs are is to know where they are used and what kind of different NFT types there are. Here are some of the most notable types of NFTs that have emerged in the past couple of years.

- Collectibles

- Artwork

- Music and Media

- Event Tickets

- Gaming

- Sport Moments

- Digital Fashion

- Memes

- Assets in Real Life

- Domains

Let’s go through the NFT types in a bit more detail.

1. Collectibles

The idea of selling collectibles is not new.

The idea of physical collectibles has moved to the NFT space. You can sell NFTs as digital trading cards or keep them as your digital collectibles.

The first example of NFT collectibles was the CryptoKitties NFT collection released in 2017. Most people also treat CryptoKitties as the first “real” use case of NFTs.

These days, there are countless NFT collections on the market.

2. Artwork

Another popular NFT type is digital art. As a matter of fact, most of the NFTs sold today are digital art. This is why some people even associate NFTs with digital art.

Digital arts, such as pictures, GIFs, and videos are sold as NFTs by artists and companies. Some of the art sold this way has been auctioned for millions of dollars. This is truly groundbreaking for artists and offers numerous opportunities for people in this field.

3. Music and Media

Music and media can be linked to NFTs. This gives true ownership of that music or media to the individual who purchases it.

In the past, music has always been a fungible good you can purchase from a store or from the internet. But tokenizing the music gives artists a whole bunch of new benefits.

- Instead of requiring a middleman, the artist has a direct reach to their loyal fanbase

- Also, now there is a way to offer a premium experience to the listeners.

- By turning music into NFTs, the artist basically gets 100% of the earnings and doesn’t have to think about the record label and streaming platform cuts.

4. Event Tickets

Another cool application for the NFTs and blockchain technology is selling event tickets as NFTs.

This works such that the organizer of a popular event mints a limited number of NFT tickets into a blockchain. Then the event goers can purchase the NFT tickets through auction listings and store the tickets in mobile wallets so that the tickets are easy to access.

Besides getting a ticket to an event, an NFT ticket can also offer additional perks, such as merch, meet-and-freets, drinks, and more.

With NFT-based ticketing, it’s much harder to fake the tickets and scam attendees. Also, the cost of selling NFT-based tickets is practically zero when compared to the traditional ticketing costs. Besides, an event goer can easily sell their NFT ticket in case they are unable to attend the event.

5. Gaming

The gaming industry has started to utilize NFT technology too! In online games, the in-game items are turned into NFTs.

The fact that an in-game item is an NFT also means there is a real-life value for that item.

Non-Fungible Tokens help build sustainable in-game economies with strong and unchangeable records of ownership for the in-game items.

Notice that the games themselves are not NFTs. But the game characters, skins, and other types of items can be.

Another common use of NFTs in the gaming industry is by selling limited edition versions of DLC assets as NFTs.

6. Sport Moments

Big sports moments are one of the trending types of NFTs big sports companies have started doing.

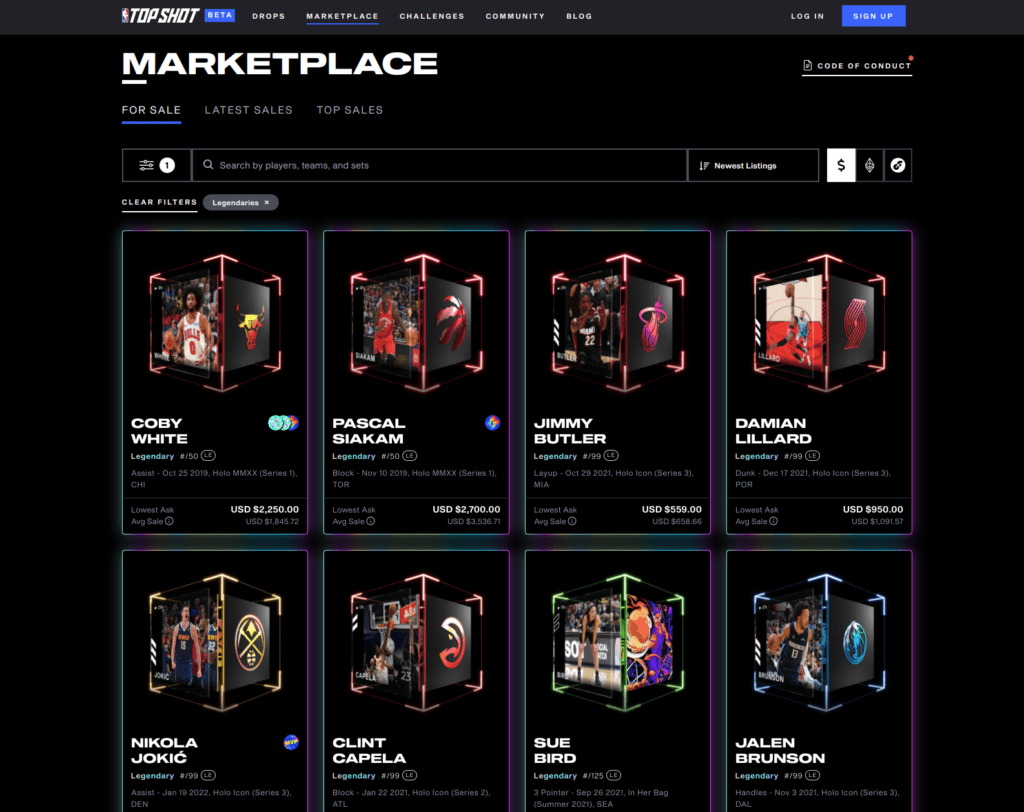

Perhaps the most famous example of this is the NBA Top Shot. It’s an NFT collection of some of the most notable NBA moments in history.

As an example, the sports moment NFTs can include legendary runs, goals, slam dunks, and so on.

7. Digital Fashion

A popular type of NFTs is NFT fashion and NFT clothing.

Naturally, you cannot wear the NFT clothing you buy online. But it’s all about personal preference on where you want to spend your money.

In some cases, you can use NFT clothing to stylize your online avatar. Needless to mention, fashion NFT hype is built around the fact that digital clothing is one-of-a-kind. No one else can purchase the same set of NFT boots you just did. And no one else’s online avatar has that kind of swag.

8. Memes

One of the most notable feats in the NFT space has been the memes sold for millions and millions of dollars.

A lot of people link memes to NFTs, although the concept of memes has nothing to do with NFTs.

The “value add” of a meme NFT is based on popularity. If a meme goes viral, everyone knows it. What would be cooler than to officially own that meme everyone knows about?

Obviously, a meme doesn’t hold real-life value. The value of the meme NFT is based on speculation and is subjective too.

9. Assets in Real Life

As stated earlier in this guide, NFTs can be almost anything. It doesn’t necessarily have to be something digital. However, whether NFTs will be effectively used with real-world items is still highly speculative and up for debate. But the advancement in the NFT space has taken promising steps toward achieving that.

The strong cryptographic proof of ownership that comes with NFTs makes it plausible to reflect real-world items. There are lots of NFT projects that focus on tokenizing luxury items and real estate. With NFT deeds, you get more options when buying a house or a car.

10. Domain Names

Besides all the different types of NFTs already mentioned, the NFT market has now made it possible to trade domains as NFTs too.

Instead of paying for a third party to manage your domain, it’s now possible to purchase one from the NFT marketplaces. The rights you get are exclusive and there is no need for a middleman to verify this. The verification of the ownership of the domain lives securely in the blockchain and is immutable.

One example of NFT domain names is the Ethereum Name Service (ENS).

NFT Pros and Cons

A great way to further understand NFTs is by taking a look at the pros and cons associated with them.

To put it short, NFTs offer a safe way to boost market efficiency, fractionalize physical assets, and add diversity to an investment portfolio.

On the other hand, NFTs are highly volatile, generate no revenue, and can be used for fraud. Besides, the technology that powers NFTs eats up huge amounts of energy and might be an environmental problem.

Here is a complete breakdown of the pros and cons related to NFTs.

Pros of NFTs

Let’s start with the pros of using NFTs to verify ownership of an asset.

1. Market Efficiency Boost

NFTs have the potential to streamline the markets. This is because NFTs allow you to convert physical assets to digital ones. This can make:

- Processes lighter

- Intermediaries unnecessary

- Supply chains stronger

- Markets more secure

By the way, there are already real-life examples of these taking place.

Take a look at the art world. Because of the rapid developments in NFT technology, an artist can easily connect with their audience without expensive agents and costly transactions. Besides, digitalizing the artwork in the form of NFT improves the authentication process. This reduces the costs even further.

Even though NFTs are known for being a reliable form of digital art, the ideology can be expanded beyond the arts. In the near future, NFTs could be used to handle sensitive data for both individuals as well as enterprises.

2. Physical Asset Fractionalization

Fractionalization of ownership of some physical assets is difficult. Think about real estate, artwork, or jewelry, for example.

Instead of dividing a physical asset with multiple owners, it’s much easier to share its digital version.

With the help of digitalization and NFTs, specific types of markets can be expanded by leaps and bounds. This can lead to better liquidity. For you, this could mean improvements in the construction of financial portfolios with better diversification and more accurate position sizing.

3. Safety

NFTs are stored in a blockchain.

Thanks to the strength of blockchain technology, the information stored is impossible to modify or delete by hackers.

In a sense, a blockchain is a digital ledger of transactions. This blockchain is duplicated and managed by the entire peer-to-peer network of participants who verify each transaction that takes place.

When you add an NFT to a blockchain, a new transaction is created to the blockchain. The information that lives inside this block cannot be modified. In other words, a hacker cannot tamper with the transactions in any way. This is what makes blockchains and NFTs so secure.

4. Potential Diversification Benefit to a Portfolio

An NFT offers a completely new way of investment as opposed to traditional investment vehicles like stocks and bonds.

It is only recently that we have started to realize the true power of NFTs when it comes to diversifying financial portfolios and making the markets better.

But investing in NFTs comes with risks! In the next section, we take a look at the cons of NFTs and touch on the risky aspects of NFTs as an investment vehicle.

Cons of NFTs

NFTs are a relatively new concept. There are many unknowns and risks associated with them too. Let’s take a look at some of the most notable cons of NFTs.

1. Volatility and Illiquidity

NFTs are making their way. But due to being in such an early stage, this sector is not liquid.

NFTs are poorly understood by consumers across the globe. Thus, there is only a handful of buyers and sellers.

This means it might be really tough to trade NFTs. This is especially true during the bad times. All this leads to high volatility where the NFT prices vary by a ton.

2. No Revenue Generation

If you are familiar with stocks, bonds, and real estate, you know that the owners of these assets get dividends, interest, and rent respectively.

But NFTs don’t generate this kind of revenue for the owners.

The return of NFT investment depends on price appreciation only. This is something you cannot affect and count on. Basically, you can only profit from NFTs if you are really lucky. NFTs offer a much less “certain” way to make money than other investment vehicles.

3. Changes in Fraud

The trustworthiness of the blockchain that powers NFTs is undeniable.

But this doesn’t remove the fact that NFTs can be used in fraudulent actions. For example, a bunch of digital artists has found their work on sale as NFTs without permission.

NFTs offer a great and less costly way to facilitate the sales of digital arts. With an NFT it’s possible to verify real works of art with a unique token to ensure the owner of the token owns the actual piece of art.

But fraudulent actions like selling without permission take us a step back.

4. Environmental Issues

It takes an unbelievable amount of computing power to sustain blockchains. This is because of the computationally heavy tasks that maintain the security of the blockchains.

This is not only a concern about NFTs. Instead, the environmental worries touch the entire blockchain and cryptocurrency space.

Studies suggest that with the continuation of current trends, blockchain technology will emit carbon as much as the whole city of London in the coming years.

Although on the other hand, enthusiasts claim that blockchain technology will transform global markets in a way that the net effect is positive. For example, blockchain technology can help reduce office space use and travel for work.

What Happens If You Take a Screenshot of an NFT?

NFT art, such as images and illustrations is commonplace. There is a chance you first heard of NFTs in the context of images or cartoon characters being sold at a high price.

But what if you take a screenshot of an NFT? Doesn’t it ruin the whole thing?

Taking a screenshot of an NFT is perfectly fine and it doesn’t have any impact on the value of the original piece.

Think about Mona Lisa. If you take a picture of this masterpiece, does it ruin the value of the original piece? It doesn’t.

By taking a screenshot of an NFT you do not become the owner of the piece. The blockchain where the NFT lives in doesn’t care about screenshots. The blockchain still has information about the owner and transaction history of the NFT.

But what if you take a screenshot of an NFT and make it a new NFT?

By using common sense, you can already tell this could lead you into trouble. If you copy someone’s work, you might be sued for copyright infringement. Besides, you still cannot ruin the value of the original piece of NFT because its metadata remains untouched in the blockchain.

To take home, screenshotting an NFT doesn’t change the ownership of the original NFT. This is because the NFT metadata remains untouched and lives securely in a blockchain.

Why Do People Buy NFTs?

People mostly buy NFTs because they can be an investment and diversify their portfolio.

The right types of NFTs might go up in price and yield a nice income. But it’s crucial to understand that evaluating the value of an NFT doesn’t work the same way you evaluate private companies or other typical investment vehicles like shares. This is because the value is typically highly speculative.

If you ever consider investing in NFTs, remember that you are probably going to lose money. NFTs are great for entertainment, but they are volatile and unpredictable.

Another reason why someone might buy an NFT is to directly support an artist. Also, someone might buy NFTs to receive a real-world token, such as an entry to an event or other perks.

In the future, it might be more real-life items are sold as NFTs. This would make it possible for individuals to buy real estate, cars, or luxury jewelry as NFTs.

Is NFT a Scam?

The concept of NFT is legit and very secure. The fact that NFTs rely on blockchain technology makes them unbreakable and safe.

Unfortunately, this doesn’t mean there wouldn’t be fraud perpetrators.

Even though NFTs are secure and legit, they can be created with bad intentions. The creator might lure people to buy their NFTs with high pricing. Because the NFT art value is based on speculations, it’s easy to attract the unsuspecting. It’s not like someone is selling a banana for $1,000. It’s more like having a legitimate person selling art at a high price.

But sometimes the creator of the NFT just takes the money and leaves you with an NFT that has no value.

If something seems too good to be true, it probably is! You must always do your research before investing in NFTs.

Can NFTs Make You Rich?

Almost always no, but in theory yes!

The NFT market is volatile and relatively new. Unless you are really lucky, chances are you will only lose money in the NFT market.

There are people who invest in NFT full-time and have never made a profit.

Especially the NFTs with a speculative value have a high potential for you to lose a lot of money.

To become rich with NFTs, you need to be lucky enough to be in the right place at the right time. But predicting the NFT markets and your potential earnings is impossible. Thus, you should use your own consideration when investing in NFTs.

How to Buy NFTs?

Last but not least, you might want to know how to actually buy NFTs.

First of all, buying cryptos and NFTs requires setting up some accounts and making some initial investments plus paying some fees. The third-party services abstract the technical parts of the process away. Thus, you don’t need to understand almost anything talked about in this guide to buy NFTs.

Keep in mind there is a reason I left this chapter toward the end of this article. NFTs won’t make you rich. As a matter of fact, you will probably only lose money by buying NFTs. Use your own discretion if you choose to buy NFTs or cryptos. Remember that the markets are volatile and unpredictable!

With that said, here are the steps to take to buy NFTs.

- Open a crypto exchange account.

- Open a crypto wallet.

- Buy Ethereum.

- Transfer the Ethereum to your crypto wallet.

- Connect your crypto wallet to an NFT marketplace.

- Buy NFT.

Here is a more thorough breakdown of the above steps.

By the way, you might find this information insightful even if you are not planning to ever buy NFTs. These steps help you understand what it takes to buy NFTs and support learning the working principle of NFTs.

1. Open a crypto exchange account

To buy an NFT, you need to open a crypto exchange account.

A crypto exchange is a brokerage in which you can buy and sell different types of cryptocurrencies.

The crypto exchange issues and holds your public keys (sometimes private keys too) for creating the digital signature with which you can interact with the blockchain.

Besides, the third-party crypto exchange keeps your cryptocurrencies safely in your account. You also get support from these services. They can help you reset your password, for example.

A commonly used crypto exchange is Coinbase.

2. Open a crypto wallet

Unlike the name suggests, a crypto wallet does not store your cryptocurrency coins or tokens. Instead, the crypto wallet stores the keys that grant access to those digital assets.

When you open up a crypto wallet, you’ll be assigned a seed phrase that you need to remember. This seed phrase is the only way you can access your wallet. If you lose the seed phrase, you can no longer access the wallet and you lose your digital assets.

You can either choose a hosted crypto wallet or operate the wallet independently. In the latter option, you have full control (and responsibility) over your wallet and the keys stored in it. On a hosted wallet, the third party holds your private keys and takes care of the security of your account and its assets.

There are lots of crypto wallet options, but MetaMask is the most popular one.

3. Buy Ethereum

Most of the NFTs live on the Ethereum blockchain.

The cryptocurrency used in the Ethereum blockchain is called Ether or ETH. But you commonly hear people calling it Ethereum too!

To buy NFT in the Ethereum blockchain, you need to buy some ETH. You can do this on the crypto exchange you signed up for in the first step.

Similar to Bitcoin, Ethereum is a cryptocurrency you can buy, sell, and save.

4. Transfer the Ethereum to your crypto wallet

Once you have purchased some ETH, it’s time to move it to your crypto wallet.

This step depends on the following factors:

- The exchange you used to buy ETH.

- The crypto wallet you use.

- The marketplace you want to buy NFTs from.

There are great online guides that teach you how to do this. For example, if you purchased ETH from Coinbase and want to transfer it to MetaMask, there are tons of tutorials showing how to do it.

But because there is no one-size-fits-all solution to this, I’m not going to show you how to do it here.

5. Connect your crypto wallet to an NFT marketplace

To buy NFTs, you need to connect your crypto wallet to an NFT marketplace. There you can use Ethereum (or other cryptocurrencies) to purchase NFTs.

These days there are lots of different NFT types you can buy from different NFT marketplaces.

The landscape of NFT marketplaces is changing rapidly and you have to keep an eye on what is relevant at the moment. But the vast majority of NFT marketplaces fall into one of three categories:

- Open marketplace. In an open marketplace, anyone can sell, buy, or mint NFTs.

- Closed marketplace. A closed marketplace is a more exclusive one. The NFT artist must apply to the marketplace. Trading NFTs is more limited in a closed NFT marketplace.

- Proprietary marketplace. A proprietary marketplace is operated by a company that has trademarked or copyrighted the NFTs they sell.

Before you head over to a marketplace, make sure to follow social media and other communication channels by interesting NFT projects or artists. The most popular channels are Twitter and Discord. Buying NFTs without doing research and being actively part of an online community doesn’t usually make sense.

Anyway, once you have chosen a couple of NFT marketplaces to join, you can connect your crypto wallet to the marketplace and start buying or selling NFTs.

The most popular NFT marketplaces include OpenSea, Rarible, SuperRare, and Nifty Gateway.

6. Buy NFT

Once you have completed all the above steps and done your research, it’s time to buy the NFTs.

Remember, the well-known NFTs with a lot of hype around them sell quickly. Make sure to connect the crypto wallet and fund the wallet before the NFT drops.

Also, keep in mind buying NFTs doesn’t automatically mean buying copyrights to the art in question. The exception is the case when there is a direct agreement between you and the creator.

Each NFT marketplace comes with its own restrictions and rules when it comes to buying NFTs.

NFT History

The year 2021 was the year of NFTs. It is at this time that the NFTs started gaining massive attention.

But the invention took place almost a decade earlier. Back in 2012, Meni Rosenfeld introduced the concept of “Colored Coins” for Bitcoin blockchains. The following years turned this concept into a massive concept called NFTs that everyone has heard about.

Here is the short historical timeline of NFTs with the key years and events.

2012-2016: The Early Days of NFTs

Back in 2012, way before the Ethereum blockchain was invented, the concept of NFTs was first thought of. Although the name wasn’t NFT. Instead, the idea was to introduce “Colored Coins” to the Bitcoin blockchain.

The idea behind a Colored Coin was very similar to the idea of Bitcoin. But besides being a currency, a Colored Coin would contain a token element to make each coin unique and irreplaceable. This would make it possible to manage real-life assets using a blockchain. Each Colored Coin would live on the Bitcoin blockchain and store information about its use.

But due to the limitations of the Bitcoin blockchain, the idea of Colored Coins never materialized. But the concept of Colored Coins laid a foundation for the invention of NFTs later on.

Two years later in 2014, Kevin McCoy minted the first ever NFT to the Namecoin blockchain. This NFT is called Quantum. It’s an image of an optical illusion caused by a pixelated octagon. Even though this is arguably the first ever NFT, it’s not that popular.

After these events, a lot of experimentation started taking place. There were lots of platforms built on top of the Bitcoin blockchain. Also, a new platform Bitcoin 2.0 or Counterparty was created. It became known as a crypto platform that allowed for the creation of digital assets. In 2016, the Rare Repes NFT was released on the Counterparty platform.

But the Bitcoin blockchain was never made to support NFTs. After the community realized this, the movement toward Ethereum took place.

2017-2020: NFTs Become Mainstream

The first widely known implementation of NFT was an NFT collection called CryptoKitties. This collection of cartoon cat images was minted to the Ethereum blockchain in 2017 using the new ERC-721 standard.

To be more precise, CryptoKitties is a game that allows players to adopt, trade, and breed digital cats and store them in a digital waller.

When this game went viral, people started trading CryptoKitties with unbelievable profits. Also, the news of this kind of new game and asset went viral. The popularity of CryptoKitties helped the word NFT take steps in becoming the next big thing in the crypto space.

After the success of CryptoKitties, NFTs combined with gaming started getting hype. The first groundbreaking NFT gaming platform was Decentraland. Decentraland is a massively popular virtual reality platform powered by the Ethereum blockchain. It’s an open-world gaming platform you can use to:

- Play different games.

- Build and collect items and other objects.

The cool part of Decentraland is that everything you own in the game you own in the Ethereum blockchain.

Lo and behold, other similar platforms appeared and allowed developers to mint their in-game items to the Ethereum blockchain. This allows players to purchase in-game items from one another using Ethereum. This, in turn, means there is also a real-world value to an in-game item. In other words, you can earn money by playing a game (Pay-to-Earn, P2E).

One example of such a game is called Axie Infinity.

2021: The Year of NFTs

During the year 2021, NFTs were already very popular and many people interested in tech and software already knew about them.

But the major breakthrough of NFTs took place in 2021. In 2021, well-known auction houses started selling NFT art. Namely, Christie’s and Sotheby’s auction houses moved online and started selling NFTs.

Also, in 2021, Christie’s record of the highest price of digital art was broken by Beeple, who sold his NFT collection for $69 million on the platform. The NFT collection Beeple sold was a collection of 5,000 images he had drawn by hand in 13+ years.

This record-breaking sale was quickly followed by new blockchains that were created to implement their own versions of NFTs. These blockchains include Cardano, Solana, Tezos, and Flow.

Also, at the end of 2021, Facebook rebranded to Meta. Furthermore, Facebook announced they will focus on the upcoming “metaverse”. This accelerated the momentum of NFTs in the metaverse even more.

Wrap Up

Today you learned what is NFT.

To recap, NFT stands for non-fungible token. An NFT is a unique token that lives inside a blockchain, usually the Ethereum blockchain. An NFT offers a secure way to prove the ownership of digital or non-digital assets. Instead of having a third party verify the ownership, the peer-to-peer network does it in a decentralized manner.

The concept of NFTs is fresh, and it needs a lot of research, innovation, and exploration. Chances are blockchain and NFTs could change the market as we know it. The NFT technology could disrupt the third parties required in transactions, such as record labels, ticketing services, art galleries, and more.

The most common type of NFT is NFT art, such as a video, image, collection of images, or GIF. People tend to buy these digital assets as NFTs to make an investment.

When it comes to NFT arts, the value of the NFT is speculative. The fact that you can become a sole owner of an asset is what draws people into it. NFTs have gained massive attention in recent years. For example, the first tweet ever was sold for $2.9 million as an NFT.

The driving forces of NFTs are unbreakable security, decentralization, and the easiness to verify transactions and ownership. On the other hand, the high volatility, environmental concerns, and fraud perpetrators cast a shadow on the industry.

Only time will tell, what the future holds for NFTs. But one thing is for sure: NFTs are here to stay!

Thanks for reading! I hope you found the information in this article useful. Make sure to share it with someone you think might find it useful!

Read Also

- Want to learn more about NFTs? Make sure to read my blog post about NFT Glossary and Terms.

- Do you want to create your own NFT collection? Make sure to check the best NFT design tools in the market.